Nol Carryback 2019 For Individuals

Wolters Kluwer United States. A taxpayer must make an election to exclude Section 965 inclusion years from the carryback period for an NOL arising in a taxable year beginning in 2018 or 2019 by the due date including extensions for filing its return for the first taxable year ending after March 27 2020.

What Are Net Operating Loss Nol Carryforwards Tax Foundation

Taxpayers can carry back NOLs includ-ing non-farm NOLs arising from tax years be-ginning in 2018 2019 and 2020 for 5 years.

Nol carryback 2019 for individuals. The election to waive the NOL carryback for NOLs arising in tax years beginning in 2018 or 2019 must be made no later than the due date including extensions for filing the taxpayers federal income tax return for the first tax year ending after March 27 2020. The 2-year carryback rule in effect before 2018 generally does not apply to NOLs arising in tax years ending after December 31 2017. However you may file an election to either waive the entire five-year carryback period or to exclude all of your section 965 years from the carryback period.

Likewise to accelerate cash flows for corporate taxpayers the CARES Act modified the AMT credit rules. A taxpayer may waive the NOL carryback for taxable years beginning in 2018 and 2019 no later than the due date. Section 13302 for tax years 2018 2019 and 2020.

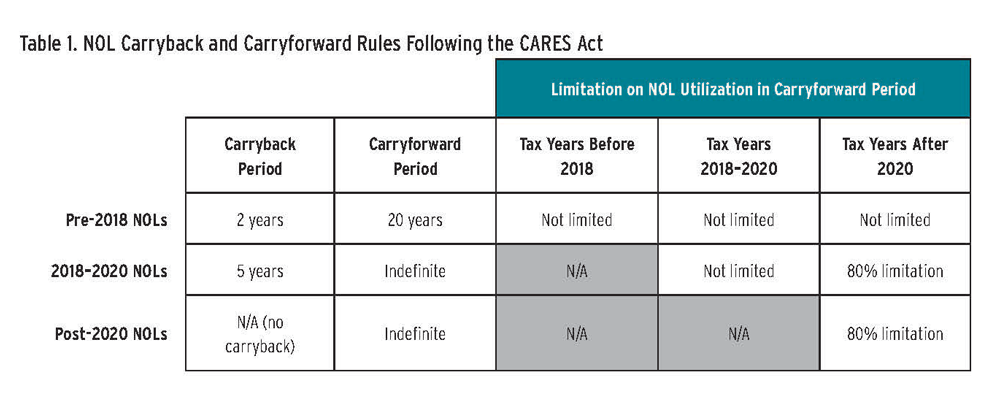

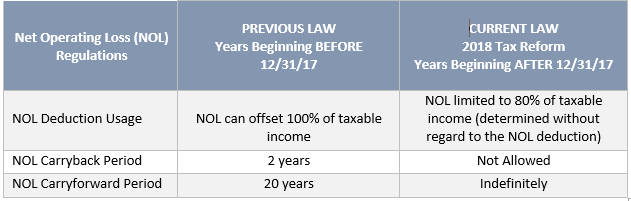

The CARES Act allows firms to carry back losses in tax years beginning after December 31 2017 and before January 1 2021 for calendar year firms covering 2018 2019 and 2020 for up to five years. Up to 10 cash back IRS Explains How Taxpayers Can Claim the Five-Year NOL Carryback Under the CARES Act. The NOL deduction for tax years beginning in 2018 2019 and 2020 will be subject to the 80 limitation starting with tax years beginning in2021.

The election is made no later than the due date including extensions for filing the taxpayers federal income tax return for the first taxable year ending after March 27 2020. Taxpayers can waive the 5-year carryback of NOLs in favor of carrying them forward with respect to. For individuals an NOL may also be attributable to casualty losses.

Exceptions apply to certain farming losses and NOLs of insurance companies. Generally you are required to carry back any NOL arising in a taxable year beginning in 2018 2019 or 2020 to each of the five taxable years preceding the taxable year in which the loss arises. Specifically a separate election to forego carrybacks may be made for each of 2018 2019 and 2020 without binding the taxpayer as to any other year.

The CARES Act also allows taxpayers to elect to exclude taxable years with a section 965 inclusion section 965 years from the carryback application of losses. Loss offsets for individuals. The Bottom Line.

They can elect to waive the carryback period and only carry these NOLs forward to future years. On the other hand the decision of whether to carry back NOLs arising in 2018 2019 or 2020 is made on a year-by-year basis. Taxpayers dont have to carryback their 2018 2019 and 2020 NOLs.

Section 2303 of the CARES Act amended the NOL carryback rules so that NOLs from taxable years beginning after December 31 2017 and before January 1 2021 can be carried back to each of the five preceding taxable years unless the taxpayer elects to forego the carryback. The CARES Act allows a taxpayer to elect to waive the five-year carryback for taxable years beginning in 2018 2019 and 2020. NOLs carried back can also offset 100 of taxable incomean increase from the 80 offset under permanent law.

Net Operating Losses. The election must be made no later than the due date including extensions for filing the taxpayers federal income tax return for the first taxable year ending after March 27 2020. Section 2303 of the CARES Act suspends the 80 of taxable income limit on NOL carryovers for 3 years.

The CARES Act provided for a special 5-year carryback for taxable years beginning in 2018 2019 and 2020. For tax years starting after December 31 2017 and before January 1 2021thats 3 calendar years of losses that you incurred in 2018 2019 or. That enhances flexibility for tax planning that did not exist before the pandemic.

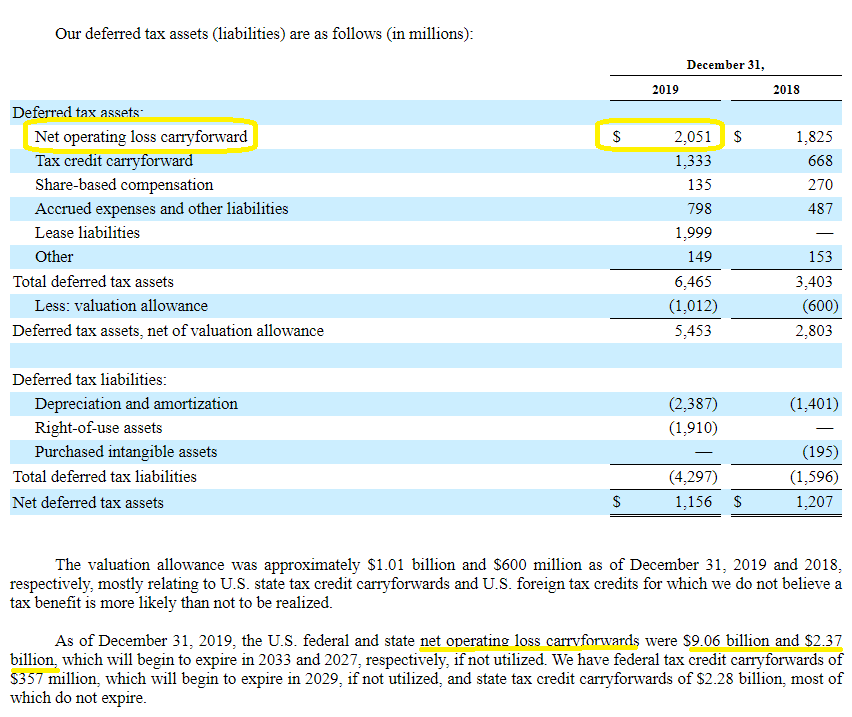

Generally a net operating loss NOL is an excess of deductions for expenses from the operation of a business over income from the operation of a business. The IRS also extended the deadline for filing an application for a tentative carryback adjustment under Sec. The IRS provided guidance on how taxpayers who want to elect to waive or reduce the new provision requiring taxpayers with net operating losses NOLs arising in tax years beginning in 2018 2019 and 2020 to carry them back five years Rev.

6411 to carry back an NOL that. Taxpayers may now use a five-year carryback for net operating losses NOLs arising in tax years beginning in 2018 2019 and 2020 compliments of the Coronavirus Aid Relief and Economic Security CARES Act PL. Under Revenue Procedure 2020-24 a taxpayer may elect to waive the carryback for NOLs arising in tax years beginning in 2018 or 2019.

For most taxpayers NOLs arising in tax years ending after 2020 can only be carried forward. Under the CARES Act a business can now carry back 100 of its net operating losses for tax years 2018 2019 and 2020 for up to five years and may claim a refund based on that adjustment for any or all taxes paid. Under the CARES Act an NOL from a tax year beginning in 2018 2019 or 2020 can be carried back five years.

The CARES Act also eliminates the 80 limitation of NOL utilization in the carryback 2013-2018 or the carryforward year 2019-2020 and allows NOLs generated for tax years 2018-2020 prior to January 1 2021 to fully offset taxable income. Waiver of the five-year carryback rule A taxpayer may elect to waive the carryback period for an NOL arising in a taxable year beginning in 2018 or 2019. In Notice 2020-26 PDF the IRS grants a six-month extension of time to file Form 1045 or Form 1139 as applicable with respect to the carryback of a net operating loss that arose in any taxable year that began during calendar year 2018 and that ended on or before June 30 2019.

Net Operating Losses Carryback Opportunities

Cares Act International Tax Implications Of Nol Rule Changes Rkl Llp

Nol Net Operating Loss Carryforward Explained Losses Become Assets

Nol Net Operating Loss Carryforward Explained Losses Become Assets

1040 Net Operating Loss Faqs Nol Schedulec Schedulee Schedulef

News Andersen Global

Net Operating Loss Nol Carryover Deduction San Jose Cpa

Nol Net Operating Loss Carryforward Explained Losses Become Assets

Cares Act International Tax Implications Of Nol Rule Changes Rkl Llp

Cares Act 5 Year Nol Carryback Example Ics Tax Llc

Nol Carrybacks Under The Cares Act Tax Executive

Cares Act Business Net Operating Loss Nol Provisions Sciarabba Walker Co Llp

What Are Good Ways To Use Your Tax Refund Tax Refund Tax Money Personal Loans

Tax Loss Carryforward How An Nol Carryforward Can Lower Taxes

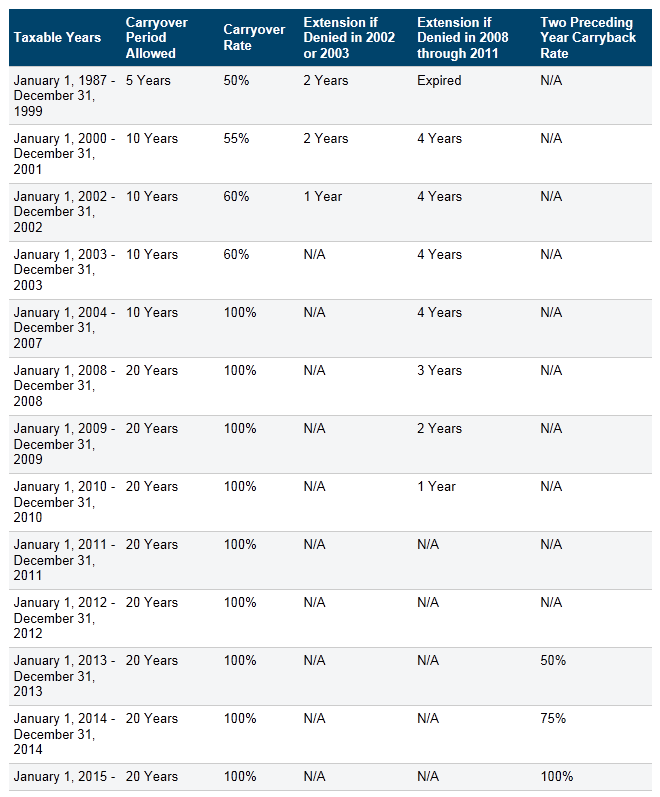

California Governor Signs Massive Package And Tax Bill

Nol Deduction Limited

Cares Act Relief May Result In Difficult Choices For Multinational Taxpayers Vinson Elkins Llp Jdsupra

1040 Net Operating Loss Faqs Nol Schedulec Schedulee Schedulef

A Small Business Guide To Net Operating Loss The Blueprint

{kind=link}

Post a Comment for "Nol Carryback 2019 For Individuals"