Election To Use Ads Depreciation

The requirement to use ADS depreciation applies both to property placed in service in years prior to the year the election is made and property placed in. The CAA is providing relief for taxpayers that made the RPTOB election and had converted the depreciation method from GDS-275 year to ADS-40 year.

Devon Bishop Age 45 Is Single He Lives At 1507 Chegg Com

The following depreciation methods are available in the program.

Election to use ads depreciation. An electing RPTB is required to use the relatively slow alternative depreciation system ADS to depreciate its residential real property non-residential real property and qualified improvement property. Listed Property used 50 or less in a qualified business. Tangible property used predominantly outside the.

The change to ADS is treated as a change in use. Electing RPTBs must use ADS depreciation for certain assets. If a taxpayer did not make these elections timely for that taxable year the Revenue Procedure allows.

Taxpayers are also allowed to make a late election to opt out of bonus depreciation make a late election to use ADS or revoke an election out of bonus depreciation by filing an amended return amended Form 1065 or AAR for the year the property was placed in service. In a year in which a taxpayer is either required to elect or voluntarily electing to use the ADS method of depreciation this can be done by completing Part III of Form 4562. 11 As a result a subsequent change to the appropriate method of depreciation under the ADS is considered a change in accounting method under Sec.

The program automatically switches to the straight-line method in the first year that it gives a larger deduction. For newly acquired covered property Rev. If you choose to use ADS for your residential rental property the election must be made in the first year the property is placed in service.

The year of change is thus the tax year in which a change in the use of the property occurs. And this election is IRREVOCABLE so even if in 2019 the LP does not generate a loss -- and thus by definition is not a syndicate -- it is still stuck with ADS depreciation and an inability to. Revenue Procedure 2019-33 PDF applies to these elections for the taxable year that includes September 28 2017.

If the taxpayer makes this election the additional first year depreciation deduction is allowable for the specified plant in the taxable year in which that plant is planted or grafted. Electing excepted trades or businesses are required to depreciate nonresidential real property residential rental property and qualified improvement property using the alternative depreciation system ADS which also makes the assets ineligible for bonus. It can also be used for non-recovery property.

While taxpayers can elect to utilize ADS most taxpayers only use ADS if they are required to do so. Again the taxpayer must file Form 3115. A farming taxpayer that properly elected to apply the exception under section 263Ad3 and applied ADS depreciation may seek a revocation of the election to avail themselves of the use of bonus depreciation and the shorter recovery periods available with GDS depreciation.

Once you make this election you can never revoke it. Taxpayers making the real property trade or business RPTOB election electing RPTOBs are required to use the alternative depreciation system ADS for residential rental property. Since bonus depreciation for 2018 is 100 this becomes even more critical to understand.

For existing properties Regs. 1168 i- 4 d provides that all depreciation must be redetermined beginning in the year the opt - out election is made resulting in a change of use. Under the Tax Cuts and Jobs Act TCJA the ADS recovery period was changed from 40 years to 30 years for residential rental property placed in service.

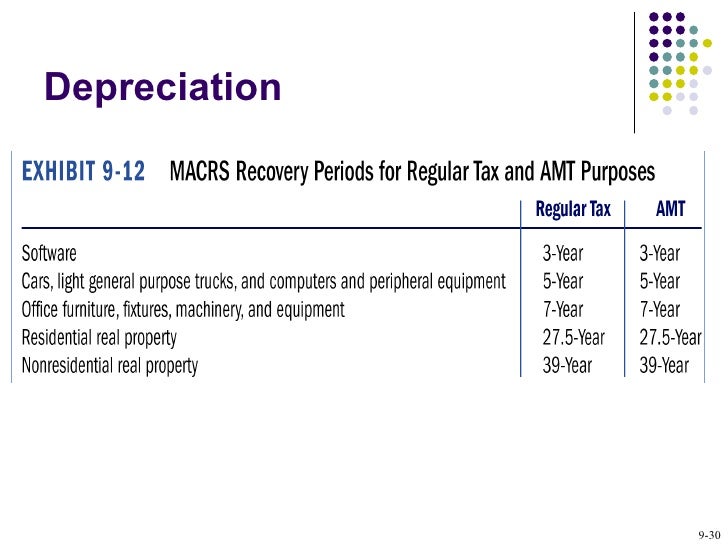

200DB - The 200 declining balance method. ADS is required in the following circumstances. This is the standard method for MACRS assets with class lives of 3 to 10 years.

For property placed in service during 2016 you make the election to use ADS by entering the depreciation on Form 4562 Part III Section C line 20c. 2019-8 provides that if the ADS is not adopted then the electing business is using an impermissible method of depreciation. In order for an electing real property trade or business to elect out of Section 163j all nonresidential real property residential rental property and qualified improvement property must be depreciated using ADS.

1163j-9 and the election is generally irrevocable once made. CAA is now allowing taxpayers that are making the RPTOB election to use ADS-30 year rather than ADS-40 year for all residential real properties that had been using GDS including those properties. Similarly an electing farming business must depreciate all property with a recovery period of 10 years or more using ADS if electing out of Section 163j.

In the year the election is made it generally is required to cover all property in the same property class that is placed in service during the year ie.

2

Depreciating Farm Property With A Seven Year Recovery Period Center For Agricultural Law And Taxation

Solved Re De Minimis Safe Harbor Regarding Multiple Busi

Depreciating Farm Property With A Seven Year Recovery Period Center For Agricultural Law And Taxation

2

Depreciation Cost Recovery Amortization And Depletion Ppt Download

Chap009

Bonus Depreciation For 2017 And Beyond

Depreciation Cost Recovery Amortization And Depletion Ppt Download

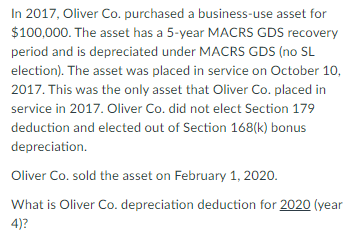

Solved In 2017 Oliver Co Purchased A Business Use Asset Chegg Com

Accounting Method Changes Post Tax Reform Ppt Download

Accounting Method Changes Post Tax Reform Ppt Download

Accounting Method Changes Post Tax Reform Ppt Download

Cost Recovery Deductions Ppt Download

Depreciation Cost Recovery Amortization And Depletion Ppt Download

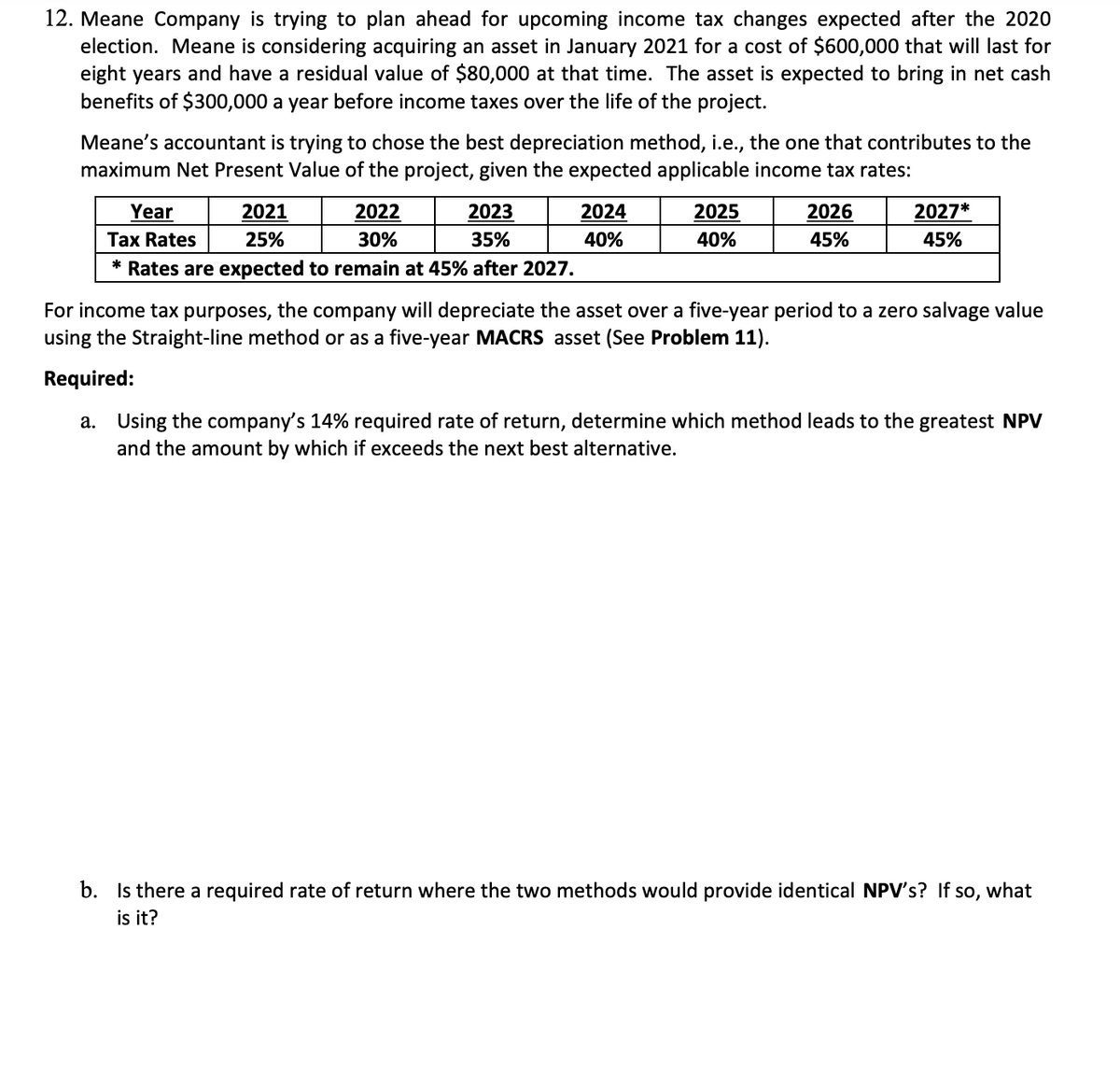

Answered 12 Meane Company Is Trying To Plan Bartleby

Accounting Method Changes Post Tax Reform Ppt Download

Cost Recovery Deductions Ppt Download

Post a Comment for "Election To Use Ads Depreciation"