What If A 754 Election Is Not Made

Citizen is a member of partnership ABC which has not previously made an election under section 754 to adjust the basis of partnership property. 3 failed to make the election because after exercising reasonable diligence taking into account the taxpayers.

Making A Valid Sec 754 Election Following A Transfer Of A Partnership Interest

What if no 754 election is made.

What if a 754 election is not made. A Section 754 election is made by the partnership not the partner and once made cannot be revoked without the consent of the IRS. Under the Section 754 regulations however an application to revoke the election will not be approved if the revocations primary purpose is to avoid stepping down the basis of partnership assets. 754 election makes it appropriate for purposes of Secs.

Section 754- Making the Election For a Section 754 Election to be valid a written statement must be attached to the partnership return and filed no later than the return due date including extensions. Further a valid Sec. Failing to make a 754 election can represent a missed opportunity for a partner to accelerate deductions and recover basis in a shorter period of time.

Late Election If the partnership fails to make the election it can file for late relief under Treasury Regulation Section 3019100-2 which is an automatic 12-month extension for IRC Section 754 elections. First it is irrevocable without consent from the IRS. This allowed us to reduce current income allocated to us and reduce taxable gain on the disposition of the partnerships assets.

754 election a qualifying transaction in the UTP creates the. Sections 754 and 743 remedy this problem. 754 to apply the provisions of Secs.

If a Section 754 election is made or in effect at the time of Xs purchase of As interest the partnership is permitted to increase the basis of its. A taxpayer will be deemed to have acted reasonably and in good faith with respect to the requested extension if the taxpayer 1 requests relief before the IRS discovers the failure to make the election. There are a few other items that should be taken into consideration before a fund makes an IRC Section 754 election.

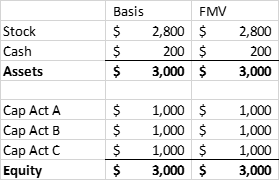

That is there is no adjustment to a transferees inside basis no adjustment to the tax basis of partnership assets because of a distribution of property by the partnership to a partner. The tax practitioner should not assume that all partnerships will have made this election or that all managing partners will want to make the election for the benefit of the partners. Once the election is in place any transaction that meets the definition of Section 743 or 734 will require a basis adjustment whether it is tax favorable or tax unfavorable.

This means that even if the LTP has not made a Sec. A Section 754 election applies to all property distributions and transfers of partnership interests during the partnership tax year for which the election is made plus for all later tax years unless revoked. The partnership and the partners use the calendar year as the taxable year.

If the partnership does not have a Section 754 election in effect at the time of the transfer it must file a statement with its partnership return for the taxable year of the partnership during. If more than 12 months have passed late relief can still be requested but must be approved by the Commissioner. The election to adjust basis on partnership transfers and distributions under 754.

Any gain recognized by the distributee because his outside basis is less than the basis of the property he received increases the basis of the remaining assets in the partnership. A few years after my mothers death the partners sold one of the properties. 754 election can only be made by the partnership.

87-115 explicitly provides that the UTPs Sec. Without making a 754 election the assets inside cost basis would be transferred to the new partner with no adjustment. The estate tax election to specially value qualified real property where the IRS has not yet begun an.

However if a 754 election is made or is in place there may be a step-up or step-down of the remaining assets. The new partner would have an inside cost basis of. 754 election on the UTP but not on the LTP Rev.

754 election is not made there is no change to the inside basis of partnership assets. The purpose of a Section 754 election is to reconcile a new partners outside and inside basis in the partnership. Two statements should be attached to the return for the taxable year during which the distribution or transfer occurs.

754 election must 1 set forth the name and address of the partnership making the election 2 be signed by any one of the partners and 3 contain a declaration that the partnership elects under Sec. 2 failed to make the election because of intervening events beyond the taxpayers control. 743b provides that in the case of a sale or exchange of a partnership interest for which a Sec.

This IRC Sec. What is 743b step up. 754 and 743 to treat the sale of an interest in the UTP as a sale of the UTPs interest in the LTP.

Once a 754 election is made it may not be revoked unless you obtain permission from the district director for the internal revenue district in which the partnership return is. When Situation 2 applies Sec. This election allows the new partner to receive the benefits of depreciation or amortization that he or she may not have received if the election was not made.

While this election can be somewhat complex and time-consuming it provides an incoming partner with a step-up or step-down in basis to reflect the FMV of the property at the time of the transfer. After consulting with a CPA we decided to make a section 754 election to step up our basis in the partnership assets.

Harry Meghan Dukeandduchessofsussexdaily Posted On Instagram Jul 11 2020 At 10 29pm Harry And Meghan News High Low Summer Dresses Meghan Markle Style

Advantages Of An Optional Partnership Basis Adjustment

Consequences Of A Section 754 Election

Avoid Costly Tax Issues By Considering The Section 754 Election Businesswest

Follow Pinterest Humor For More Funny Pictures Funny Quotes Via Http Pinteresthumor Com Funny Animal Pictures Funny Animals Animals

What Is A 754 Election Wolters Kluwer

Germany Election Olaf Scholz S Social Democrats Come Out On Top But Smaller Parties Hold The Key To Government

Could The 754 Election Benefit Your Partnership Ds B

2

Partnership Taxation What You Should Know About Section 754 Elections

Partnership Taxation What You Should Know About Section 754 Elections

Pin On Saints And Feast Days Of The Liturgical Year

Consequences Of A Section 754 Election

Advantages Of An Optional Partnership Basis Adjustment

Partnership Taxation What You Should Know About Section 754 Elections

Consequences Of A Section 754 Election

Pin On Christian Memes

29 Fourth Of July Recipes Your Kids Will Love Desserts Holiday Treats Sugar Cookies

Irc 754 Elections And Basis Adjustments Under Irc 734 And 743 Wealthcounsel Quarterly Volume 10 Issue 3

{kind=link}

Post a Comment for "What If A 754 Election Is Not Made"