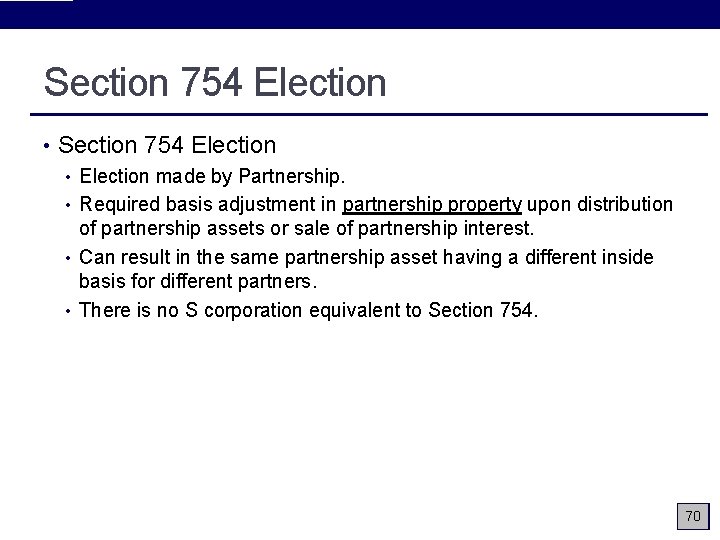

How Does A Partnership Make A 754 Election

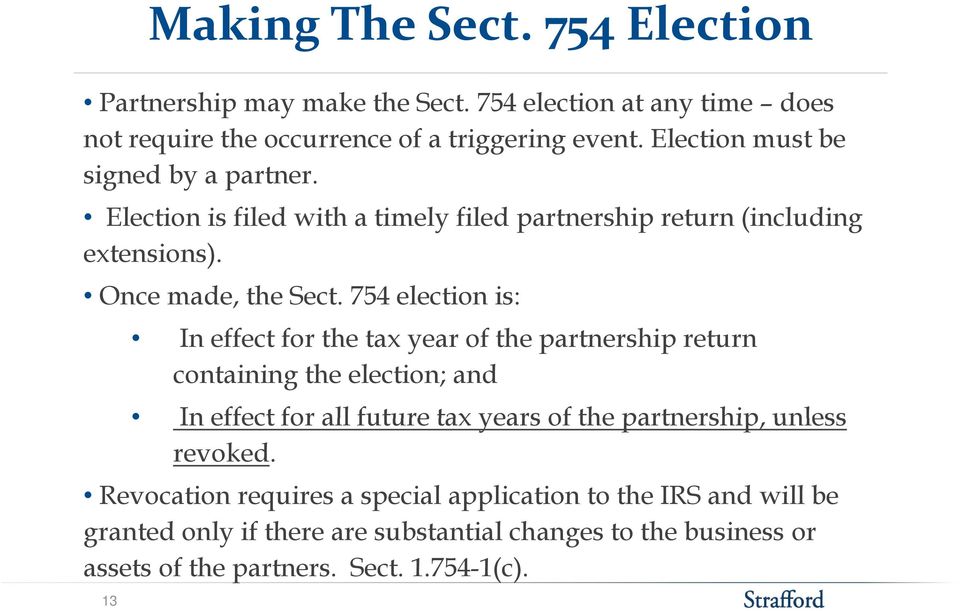

It must be made before the due date of the income tax return including extensions for the year that the transfer occurs. At a high level the purpose of the Section 754 election is to align inside and outside basis to avoid these scenarios.

Advantages Of An Optional Partnership Basis Adjustment

If the partnership decides they want the step-up they must make the 754 election.

How does a partnership make a 754 election. In other words the partnership will step up or step down its basis in partnership property when a specific eventa property distribution or the transfer of a partnership interestoccurs. Consider the following scenario. A 754 election is made at the partnership level.

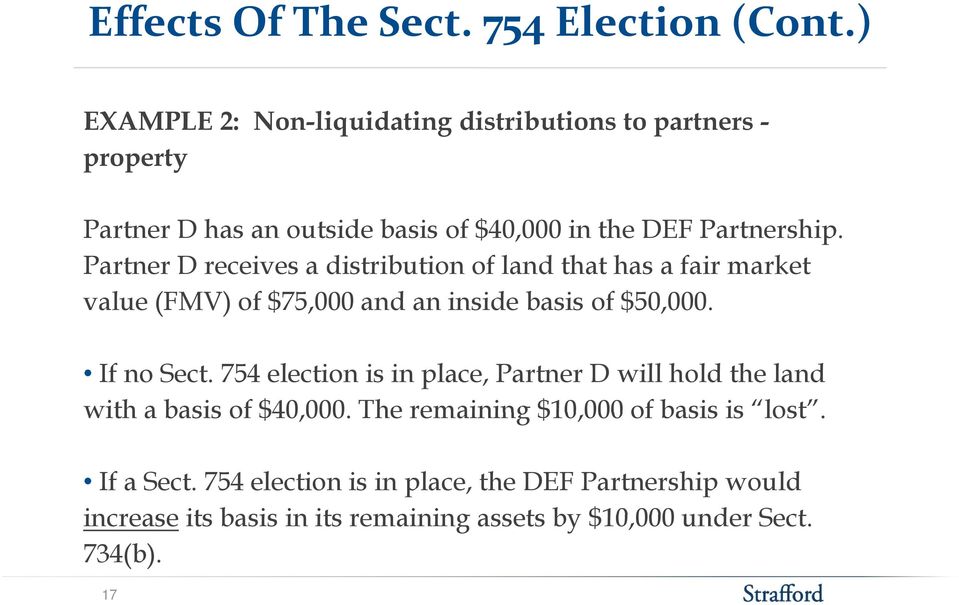

Click to see full answer. Situations Where a Basis Adjustment Can Be Made. If a Section 754 election were in place the partnership would be required to reduce the tax basis of its land specific to X by the excess of Xs share of the inside basis of the assets.

754 to apply the provisions of Secs. Further a valid Sec. A sells his interest in the partnership to D on January 1 1971.

754 to apply the provisions of Secs. At this time ATX does not support the automatic calculation of Section 754 elections. 743b upon the transfer of a partnership interest caused by a partners death.

The basis adjustment is available even if subsequent payments will be made as part of an installment sale. This allowed us to reduce current income allocated to us and reduce taxable gain on the disposition of the partnerships assets. Go to Page 3.

754 provides an election to adjust the inside bases of partnership assets pursuant to Sec. 754 election can also be made when a members interest is sold or upon certain distributions of partnership assets. 1014 a 1.

Go to Form 1065. If a section 754 election is in effect the purchasing partners have a basis adjustment under Section 743b in their respective share of the basis of the partnerships assets that generally simulates a purchase of assets. This balances the inside cost basis and outside cost basis and reduces capital gains tax when a property that has appreciated is sold.

This is done by adjusting the partnerships basis in those assets inside basis to align with the partners basis in the partnership outside basis. A partnership agreement would be a common place to contain a statement regarding this tax election but it could also be placed in a resolution adopted by the partnership or simply be contained on a tax form. Statement of Section 754 Election i.

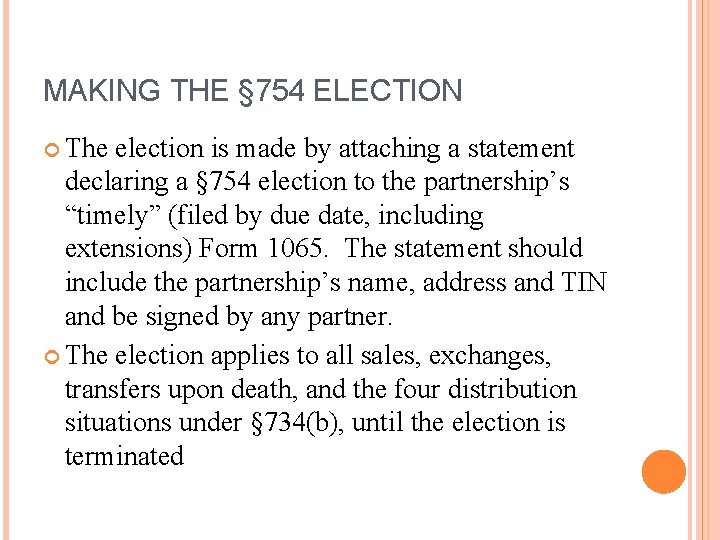

See the regs as well. The partnership needs to attachthe corresponding signed forms to the income tax return. 754 election must 1 set forth the name and address of the partnership making the election 2 be signed by any one of the partners and 3 contain a declaration that the partnership elects under Sec.

Select the Ln 13d Sch K - Oth Ded tab. How do you make a section 754 election. How and Why to Make a 754 Election.

The partnership and the partners use the calendar year as the taxable year. 754 election must 1 set forth the name and address of the partnership making the election 2 be signed by any one of the partners and 3 contain a declaration that the partnership elects under Sec. A few years after my mothers death the partners sold one of the properties.

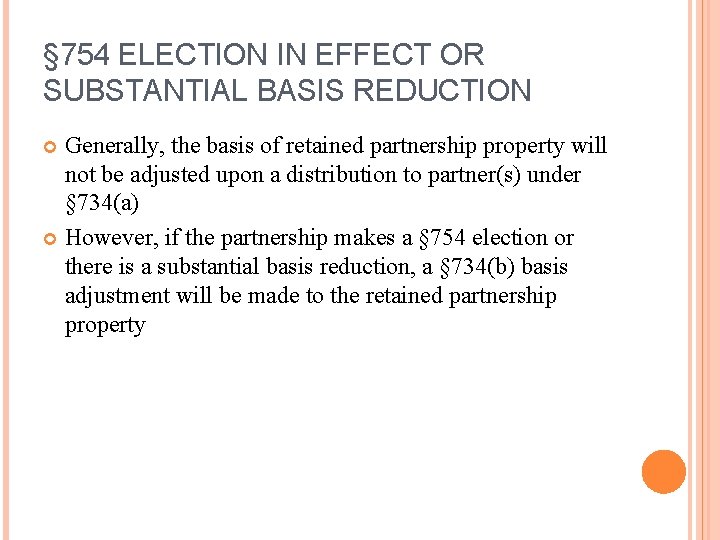

To remedy this a partnership may make a 754 election under Internal Revenue Code sections 743 b and 734 b to equalize the buyers basis in the purchased partnership interest in property outside basis and the buyers share of the basis of the assets inside the partnership net of liabilities inside basis. Generally a person receiving a partnership interest upon the death of a partner receives that interest with a basis equal to the fair market value of the interest immediately before the partners death plus any assumed partnership liabilities. Select the Yes check box on Line 12a - Is the partnership making or had it previously made and not revoked a section 754 election.

This should be 743 b ANDOR 734 b whichever applies Sec. Two statements should be attached to the return for the taxable year during which the distribution or transfer occurs. After consulting with a CPA we decided to make a section 754 election to step up our basis in the partnership assets.

754 election to adjust basis under 743 b or 734 b. Its absence from the partnership agreement does not prohibit making one but does not compel the partnership to make this election either. You make a Sec.

755 details below how basis should be allocated. Section 754 allows a partnership to make an election to step-up the basis of the assets within a partnership when one of two events occurs. Further a v alid Sec.

To enter Section 754 elections do the following. 734 b and 743 b. The partnership may elect under section 754 and this section to adjust the basis of partnership property under sections 734 b and 743 b.

Section 754- Making the Election For a Section 754 Election to be valid a written statement must be attached to the partnership return and filed no later than the return due date including extensions. When a 754 election is made the partnership steps up the inside cost basis but only for the new partner. This step-up in basis is used to make the outside basis basis of the partnership in the hands of the owner equal to the inside basis the basis of the assets in partnership for tax.

754 to apply the provisions of Secs. Distribution of partnership property or transfer of an interest by a partner. A Section 754 election applies to all property distributions and transfers of partnership interests during the partnership tax year for which the election is made plus for all later tax years unless revoked.

754 election must 1 set forth the name and address of the partnership making the election 2 be signed by any one of the partners and 3 contain a declaration that the partnership elects under Sec.

Partnership And S Corporation Differences Fort Worth Cpa

Section 754 And Basis Adjustments Pdf Free Download

Section 754 And Basis Adjustments Pdf Free Download

![]()

Partnerships And S Corporations Ppt Download

Making A Valid Sec 754 Election Following A Transfer Of A Partnership Interest

An Alternate Route To An Ipo Up C Partnership Tax Considerations Part 2

Section 754 And Basis Adjustments Pdf Free Download

Chapter 13 Basis Adjustments To Partnership Property Basis

Section 754 And Basis Adjustments For Partnership And Llc Interests

Section 754 Elections Theory Practice Youtube

Partnership Taxation What You Should Know About Section 754 Elections

Chapter 13 Basis Adjustments To Partnership Property Ppt Download

Partnership Basis Adjustments

Partnership Taxation What You Should Know About Section 754 Elections

Section 754 And Basis Adjustments Pdf Free Download

Chapter 13 Basis Adjustments To Partnership Property Basis

Advantages Of An Optional Partnership Basis Adjustment

Chapter 13 Basis Adjustments To Partnership Property Basis

Gifts Of Partnership Interests

{kind=link}

Post a Comment for "How Does A Partnership Make A 754 Election"