Business Nol Carryback Rules

Are there any limitations on which corporate taxpayers can. A NOL may be present when the taxpayers deductions exceed his adjusted gross income and result in a negative taxable income.

Cares Act Business Income Tax Implications Opportunities Rkl Llp

The rules for NOLs arising in tax years beginning after Dec.

Business nol carryback rules. You may be able to claim your loss as an NOL deduction. This means the NOL cant reduce your taxes to zero when you carry a NOL forward to future years. Rather the business owes no income tax in that tax year and the loss can be carried forward indefinitely.

To have an NOL your loss must generally be caused by deductions from your. If your deductions and losses are greater than your income from all sources in a tax year you may have a net operating loss NOL. An election may be made to waive the carryback period.

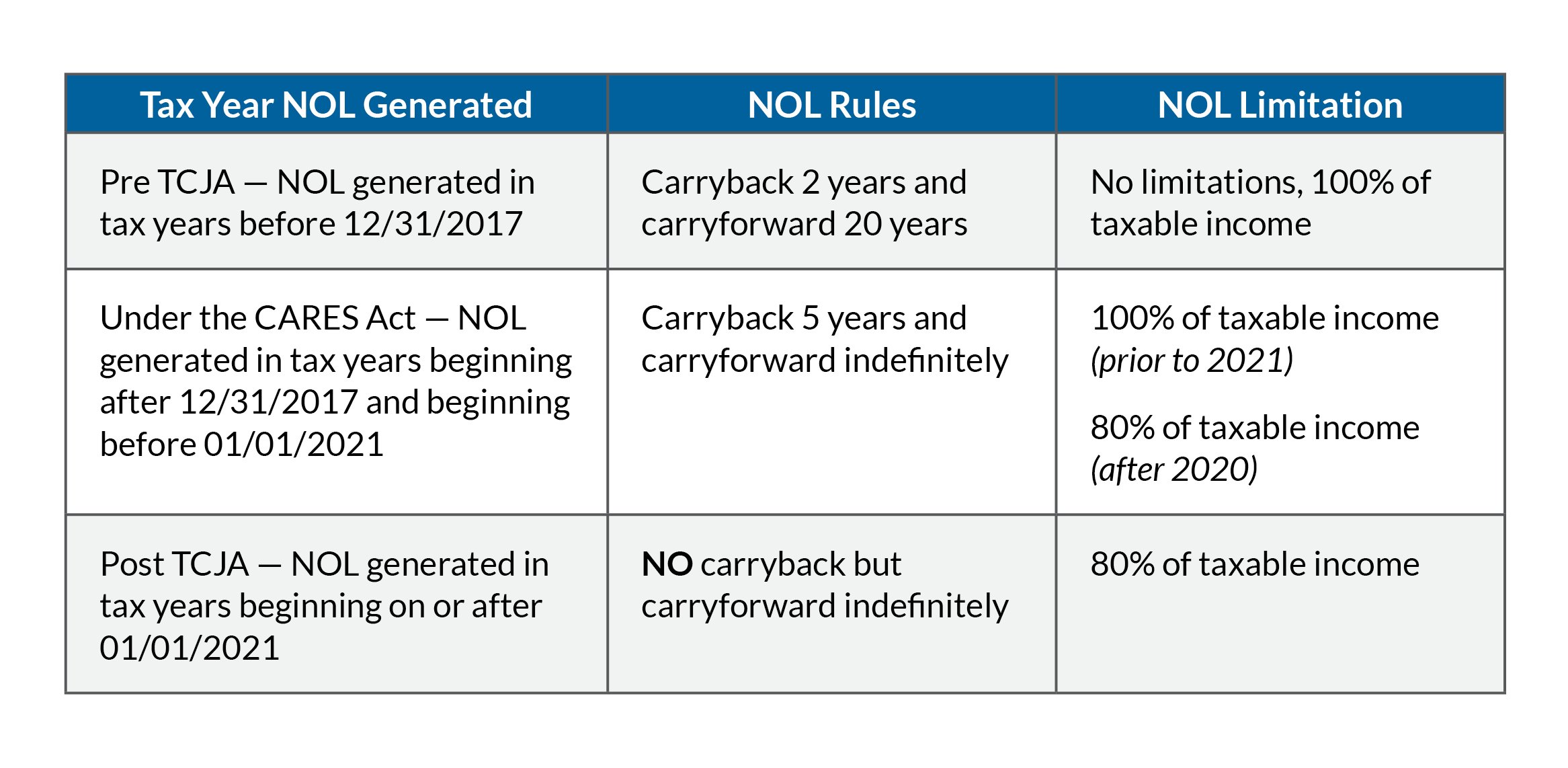

Questions and Answers about NOL Carrybacks of C Corporations to Taxable Years in which the Alternative Minimum Tax Applies. The Coronavirus Aid Relief and Economic Security Act CARES Act amended section 172 b 1 to provide for a carryback of any net operating loss NOL arising in a taxable year beginning after December 31 2017 and before January 1 2021 to each of the five. With many businesses experiencing losses due to COVID-19 now is a good time to review the CARES Act net operating loss NOL rules.

The Act provides a special rule for filing a carryback claim for the 2018 tax year and certain fiscal or short-tax years which will deem a carryback claim timely filed if it. Under current permanent law enacted in the TCJA and effective in 2018 when a firm has a loss a net operating loss or NOL taxes are not reduced immediately beyond zero. The amount of net operating loss disallowed as a deduction for a taxable year because of the foregoing limitation may be carried forward to one or more subsequent taxable years to the extent allowed under the carry forward rules of 830 CMR 63302 5.

31 2017 and before Jan. Site is Updated Continuously. Includes Editors Notes Written by Expert Staff.

Under 172 of the Code if the taxpayer has a NOL it can be used as a NOL deduction which can be carried back or carried forward and used to offset taxable income in carryback or carryforward year. The NOL changes were one of the primary revenue raisers in the TCJA to help offset the cost of lowering the corporate income tax. NOLs arising in tax years beginning in 2018 2019 and 2020 may be carried back for a period of five years and carried forward indefinitely.

For taxpayers with NOLs arising in taxable years beginning on or after January 1 2018 and ending before March 27 2019 the deadline to file an application for a tentative refund as a result of the carryback of such NOLs had. However these NOLs can now be. You can carry your NOL forward to any number of future years until it is used up.

Cess business loss limitation rule so the NOL carryback will not exceed 262000 524000 for joint returns. The corporation may establish an NOL carryforward balance under the GCT that reflects the NOLs it incurred while a taxpayer in the City and it must determine that balance as if it used the greater of i the NOLs it would have used under the GCT and ii the NOLs it effectively used under the Business Corporation Tax Subchapter 3-A. 31 2017 are modified such that a corporations NOL carryover can only offset 80 percent of taxable income without regard to the new section 199A deduction.

The NOL carryback rules also apply to individuals estates and trusts and tax-exempt organizations filing Form 990-T Exempt Organization Business Income Tax Return to report unrelated business taxable income. Ad Bloomberg Tax Offers Full-Text of the Current Internal Revenue Code Free of Charge. Trade or business Work as an employee Casualty and theft losses Moving expenses or Rental property.

Property and casualty insurance companies. If the NOL is still not used up in the first year prior to the NOL year carry the remaining amount forward one year after the NOL year. A loss from operating a business is the most common reason for an NOL.

Applies to insurance companies other than a life insurance company and an NOL has a 2-year carryback period. For individuals an NOL may also be attributable to casualty losses. Back for NOLS and suspend the 80 carryforward limitation for tax years beginning after December 31 2017 and before January 1 2021 2018 2019 and 2020 12.

COVID Relief for taxpayers claiming NOLs. An added benefit exists since the corporate equity reduction transaction rules of section 172h were repealed with the TCJA meaning it is more likely that the full amount of NOLs should be available for the five-year carryback. The net operating loss NOL carryback rules have changed over time frequently becoming more taxpayer favorable during times of economic crises.

The Tax Cuts and Jobs Act TCJA changed the rules for deducting net operating losses in 2017. The TCJA eliminated the rules allowing a two-year carryback of NOLs while allowing for the indefinite carryforward of NOLs beginning in tax year 2018. Revenue Procedure 2020-24 PDF provides guidance to taxpayers with net operating losses that are carried back under the CARES Act by providing procedures for.

For example if only 2000 of the 4000 carried to 2012 was used up you carry the remaining 2000 to 2014 one year after the NOL year. This deduction can be carried back to the past 2 years andor you can carry it forward to future tax years. As a result businesses may amend their federal 2018 tax year returns to carryback current year losses and offset federal taxable income for tax years as far back as 2013.

Generally a taxpayer must file Form 1139 or Form 1045 within 12 months of the close of the taxable year in which an NOL arises to apply for a tentative refund based on the NOL carryback. Before 2017 NOLs were fully deductible and could be carried back two years and carried forward 20 years. Generally a net operating loss NOL is an excess of deductions for expenses from the operation of a business over income from the operation of a business.

However you are allowed to deduct NOLs only up to 80 of taxable income for the carryforward years not counting the NOL deduction. Waiving the carryback period in the case of a net operating loss arising in a taxable year beginning after Dec. In subsequent years the NOL.

1 2018 the Tax Cuts and Jobs Act TCJA changed the historic NOL carryback rules. Effective for tax years beginning Jan. Farmers can still carryback losses from 2018 and 2019 and this carryback is limited to two years.

Nol Procedures Under The Cares Act Offer Tax Saving Opportunities Gyf

/business-people-using-pen-tablet-notebook-are-planning-a-marketing-plan-to-improve-the-quality-of-their-sales-in-the-future--881542122-b474ce4102d044c2b11c3a50709ec44d.jpg)

Loss Carryback Definition

Net Operating Losses After The Tcja Sciarabba Walker Co Llp

Covid 19 Tax Guidance For Businesses Journal Of Accountancy

News Andersen Global

Most People Are Upset About More Debt Investors Are Cheering In Their Homes Https Finance Yahoo Co Real Estate Quotes Small Business Loans Being A Landlord

Corporate Net Operating Loss Carryforward And Carryback Provisions By State Tax Foundation

Hidden Stimulus In The Cares Act For Businesses Net Operating Loss Carrybacks Can Bring Sweet Returns

Cares Act Cash Tax Refund Opportunities For Corporations

Corporate Net Operating Loss Carryforward And Carryback Provisions By State Tax Foundation

Cares Act Net Operating Loss Nol Provisions Corporate Taxpayers Sobelco

Cares Act Business Net Operating Loss Nol Provisions Sciarabba Walker Co Llp

A Small Business Guide To Net Operating Loss The Blueprint

Cares Act Business Income Tax Implications Opportunities Rkl Llp

Relief For Businesses With Net Operating Losses Abip

2

Corporate Net Operating Loss Carryforward And Carryback Provisions By State Tax Foundation

Cares Act Nol Deduction Changes Dalby Wendland Co P C

Nol Carryback Rules Under The Cares Act Cssi

{kind=link}

Post a Comment for "Business Nol Carryback Rules"